加密貨幣是近年來很熱門的課題,我們這次就來看看如何用簡單實作量化交易的整個流程,在這個教學裡面會一次展示如何爬取資料,算出一大堆技術指標(目前大約150個),然後設計一個交易策略,在歷史data以及線上交易上做回測,用這個策略自動交易。

基本設定

首先,安裝和設定環境,大家可以在colab上嘗試:

pip install cryptota -U接下來做一些基本設定,我們這次用ADA作為我們的範例

# Fetch data setting

CRYPTO = "ADAUSDT"

START = '7 day ago UTC'

END = 'now UTC'

INTERVAL = '1m'

# trading strategy parameter

PARAMETER = { "initial_state": 1, "delay": 500, "initial_money": 100,"max_buy":10, "max_sell":10 }

# binance api key and secret

APIKEY = ""

APISECRET = "環境設定

import cryptota

import vectorbt as vbt

import numpy as np

from binance import Client, ThreadedWebsocketManager, ThreadedDepthCacheManager

import matplotlib.pyplot as plt

import time

from datetime import timedelta

client = Client(APIKEY,APISECRET)

UNITS = {"s":"seconds", "m":"minutes", "h":"hours", "d":"days", "w":"weeks"}

def convert_to_seconds(s):

count = int(s[:-1])

unit = UNITS[ s[-1] ]

td = timedelta(**{unit: count})

return td.seconds + 60 * 60 * 24 * td.days資料取得

把資料拿下來,算指標

binance_data = vbt.BinanceData.download(

CRYPTO,

start=START,

end=END,

interval=INTERVAL

)

price = binance_data.get()

ta = cryptota.TA_Features()

df_full = ta.get_all_indicators(price.copy())

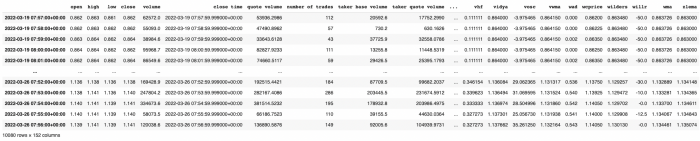

直接看看得到的指標和資料

有資料和指標,我們就可以設計自己的策略

def buy_stock(

real_movement,

delay = 5,

initial_state = 1,

initial_money = 10000,

max_buy = 1,

max_sell = 1,

print_log=True

):

"""

real_movement = actual movement in the real world

delay = how much interval you want to delay to change our decision from buy to sell, vice versa

initial_state = 1 is buy, 0 is sell

initial_money = 1000, ignore what kind of currency

max_buy = max quantity for share to buy

max_sell = max quantity for share to sell

"""

starting_money = initial_money

delay_change_decision = delay

current_decision = 0

state = initial_state

current_val = real_movement[0]

states_sell = []

states_buy = []

states_entry = []

states_exit = []

current_inventory = 0

def buy(i, initial_money, current_inventory):

shares = initial_money // real_movement[i]

if shares < 1:

if print_log:

print(

'day %d: total balances %f, not enough money to buy a unit price %f'

% (i, initial_money, real_movement[i])

)

else:

if shares > max_buy:

buy_units = max_buy

else:

buy_units = shares

initial_money -= buy_units * real_movement[i]

current_inventory += buy_units

if print_log:

print(

'day %d: buy %d units at price %f, total balance %f'

% (i, buy_units, buy_units * real_movement[i], initial_money)

)

states_buy.append(0)

return initial_money, current_inventory

if state == 1:

initial_money, current_inventory = buy(

0, initial_money, current_inventory

)

for i in range(0, real_movement.shape[0], 1):

sentry = False

sexit = False

if real_movement[i] < current_val and state == 0:

if current_decision < delay_change_decision:

current_decision += 1

else:

state = 1

initial_money, current_inventory = buy(

i, initial_money, current_inventory

)

current_decision = 0

states_buy.append(i)

sentry = True

if real_movement[i] > current_val and state == 1:

if current_decision < delay_change_decision:

current_decision += 1

else:

state = 0

if current_inventory == 0:

if print_log:

print('day %d: cannot sell anything, inventory 0' % (i))

else:

if current_inventory > max_sell:

sell_units = max_sell

else:

sell_units = current_inventory

current_inventory -= sell_units

total_sell = sell_units * real_movement[i]

initial_money += total_sell

try:

invest = (

(real_movement[i] - real_movement[states_buy[-1]])

/ real_movement[states_buy[-1]]

) * 100

except:

invest = 0

if print_log:

print(

'day %d, sell %d units at price %f, investment %f %%, total balance %f,'

% (i, sell_units, total_sell, invest, initial_money)

)

current_decision = 0

states_sell.append(i)

sexit = True

states_entry.append(sentry)

states_exit.append(sexit)

current_val = real_movement[i]

invest = ((initial_money - starting_money) / starting_money) * 100

total_gains = initial_money - starting_money

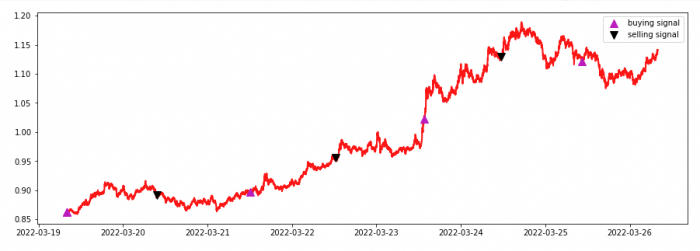

return states_buy, states_sell,states_entry,states_exit, total_gains, invest這個策略的成效如何呢,我們拿歷史data測試看看

states_buy, states_sell, states_entry, states_exit, total_gains, invest = buy_stock(df_full.close,**PARAMETER)

畫成圖表來看看

close = df_full['close']

fig = plt.figure(figsize = (15,5))

plt.plot(close, color='r', lw=2.)

plt.plot(close, '^', markersize=10, color='m', label = 'buying signal', markevery = states_buy)

plt.plot(close, 'v', markersize=10, color='k', label = 'selling signal', markevery = states_sell)

plt.legend()

plt.show()

交易其實還有手續費,高頻交易時也要考慮看看

fees = 0.001

try:

fees = client.get_trade_fee(symbol=CRYPTO)[0]['makerCommission']

except:

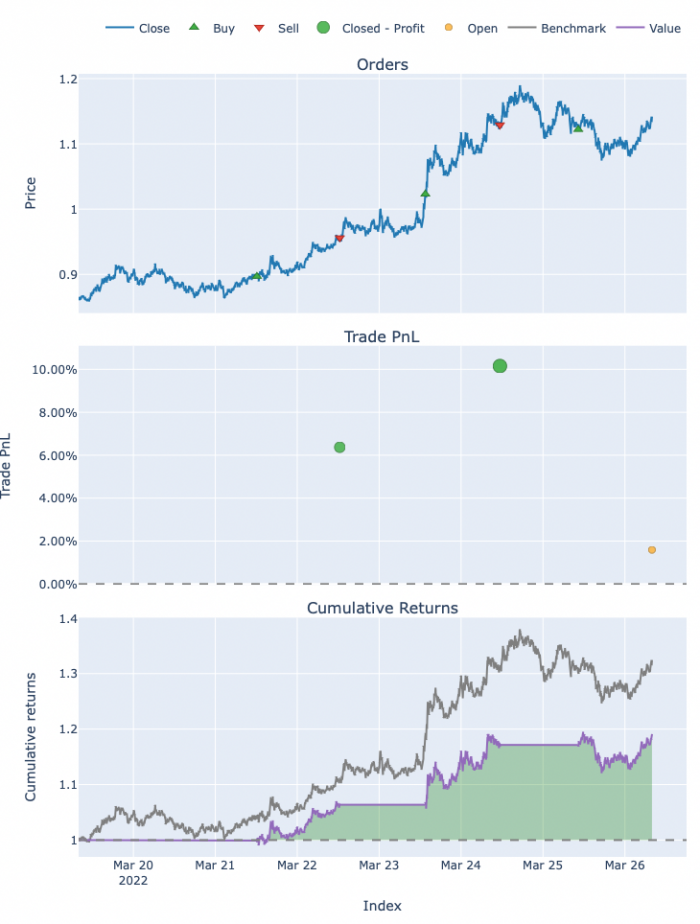

pass然後我們再看看更詳細的回測成效

portfolio_kwargs = dict(size=np.inf, fees=float(fees), freq=INTERVAL)

portfolio = vbt.Portfolio.from_signals(df_full['close'], states_entry, states_exit, **portfolio_kwargs)

portfolio.plot().show()

portfolio.stats()Start 2022-03-19 07:57:00+00:00

End 2022-03-26 07:56:00+00:00

Period 7 days 00:00:00

Start Value 100.0

End Value 119.015983

Total Return [%] 19.015983

Benchmark Return [%] 32.366589

Max Gross Exposure [%] 100.0

Total Fees Paid 0.546932

Max Drawdown [%] 6.113537

Max Drawdown Duration 1 days 03:33:00

Total Trades 3

Total Closed Trades 2

Total Open Trades 1

Open Trade PnL 1.864827

Win Rate [%] 100.0

Best Trade [%] 10.15132

Worst Trade [%] 6.370903

Avg Winning Trade [%] 8.261111

Avg Losing Trade [%] NaN

Avg Winning Trade Duration 0 days 23:04:00

Avg Losing Trade Duration NaT

Profit Factor inf

Expectancy 8.575578

Sharpe Ratio 12.557528

Calmar Ratio 143196.901926

Omega Ratio 1.079802

Sortino Ratio 18.805026

Name: close, dtype: object一旦找到合適的策略,我們就可以將他上線了

先確定看看資訊

info = client.get_symbol_info(CRYPTO)

info{'allowTrailingStop': False,

'baseAsset': 'ADA',

'baseAssetPrecision': 8,

'baseCommissionPrecision': 8,

'filters': [{'filterType': 'PRICE_FILTER',

'maxPrice': '1000.00000000',

'minPrice': '0.00100000',

'tickSize': '0.00100000'},

{'avgPriceMins': 5,

'filterType': 'PERCENT_PRICE',

'multiplierDown': '0.2',

'multiplierUp': '5'},

{'filterType': 'LOT_SIZE',

'maxQty': '900000.00000000',

'minQty': '0.10000000',

'stepSize': '0.10000000'},

{'applyToMarket': True,

'avgPriceMins': 5,

'filterType': 'MIN_NOTIONAL',

'minNotional': '10.00000000'},

{'filterType': 'ICEBERG_PARTS', 'limit': 10},

{'filterType': 'MARKET_LOT_SIZE',

'maxQty': '8005213.92147324',

'minQty': '0.00000000',

'stepSize': '0.00000000'},

{'filterType': 'MAX_NUM_ORDERS', 'maxNumOrders': 200},

{'filterType': 'MAX_NUM_ALGO_ORDERS', 'maxNumAlgoOrders': 5}],

'icebergAllowed': True,

'isMarginTradingAllowed': True,

'isSpotTradingAllowed': True,

'ocoAllowed': True,

'orderTypes': ['LIMIT',

'LIMIT_MAKER',

'MARKET',

'STOP_LOSS_LIMIT',

'TAKE_PROFIT_LIMIT'],

'permissions': ['SPOT', 'MARGIN'],

'quoteAsset': 'USDT',

'quoteAssetPrecision': 8,

'quoteCommissionPrecision': 8,

'quoteOrderQtyMarketAllowed': True,

'quotePrecision': 8,

'status': 'TRADING',

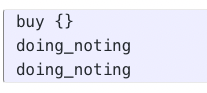

'symbol': 'ADAUSDT'}這裡就用一個最簡單的loop自動交易, 我們的策略會按照當前的data判斷是否買賣,需要的話就自動買賣。

while True:

binance_data = binance_data.update()

price = binance_data.get()

states_buy, states_sell, states_entry, states_exit, total_gains, invest = buy_stock(price.Close,

initial_state = 1,

delay = 10,

initial_money = 1,

max_buy=1,

max_sell=1,

print_log=False)

states_entry[-1],states_exit[-1]

if not (states_entry[-1] or states_exit[-1]):

print("doing_noting")

if states_entry[-1]:

order = client.create_test_order( ## use test_order for real~

symbol='ADAUSDT',

side=Client.SIDE_BUY,

type=Client.ORDER_TYPE_MARKET,

quantity=8)

print("buy",order)

if states_exit[-1]:

order = client.create_test_order( ## use test_order for real~

symbol='ADAUSDT',

side=Client.SIDE_BUY,

type=Client.ORDER_TYPE_MARKET,

quantity=8)

print("sell",order)

time.sleep(convert_to_seconds(INTERVAL))

完整程式碼: https://voidful.dev/jupyter/2021/02/20/cryptotaipynb.html